Today, a word or two in praise of sludge, the fudge we cannot budge, the smudge we cannot nudge.

Sludge perplexes with complexity as it dazzles with carbon-negative opportunity. Abundant, cheap, unstoppable, impervious to the supply curves of economists, and disdainful of the attempts of landfillers to contain it. It has nowhere to go, and cannot stay where it is. In short we must move it everywhere and cannot move it anywhere. And don’t get me started on those ‘forever chemical’ PFASs in there. A more perfect candidate for bioconversion one could not find in all the living world. Yes, in Digestville, we never begrudge sludge.

For the love of sludge and the carbon possibilities, I have long kept an eye on Aries Clean Technology and it has not been an easy ride for this company in its journey to first commercial. We reported on its progress last autumn, here. But Aries might just have it, and maybe this year.

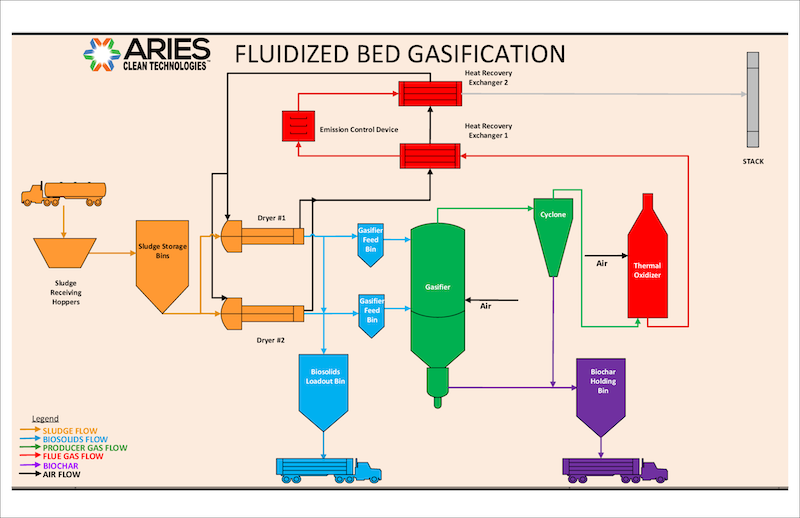

Now, one point to make, in today’s column, I’m looking at its fluidized bed gasification technology. In this one, sludge is dried from 80{7bfcd0aebedba9ec56d5615176ab7cebc5409dfb82345290162ba6c44abf8bc8} water to a 20{7bfcd0aebedba9ec56d5615176ab7cebc5409dfb82345290162ba6c44abf8bc8} water content biosolid, which is then fed to the Aries gasifier, which generates syngas (for heat and power use, for example), and 5{7bfcd0aebedba9ec56d5615176ab7cebc5409dfb82345290162ba6c44abf8bc8} of the original biosolid becomes bio fly-ash.

The first commercial is located in Linden, New Jersey. Here are the local benefits as Aries sees them.

Local Benefits

- Diverts 130,000 tons of biosolids from landfills annually

- Lowest cost option for biosolids disposal in NY/NJ Metropolitan area

- System is carbon negative and captures methane (with a global warming impact 23 times greater than CO2) that would otherwise be released into the atmosphere

- Reduce Greenhouse Gases due to reduction in trucking miles of conventional disposal methods

- Aries’ Build-Own-Operate model provides no financial risk to Linden Roselle Sewerage Authority

- Host Community Benefits to City of Linden

- Serving the largest metropolitan area in the US – The New York metropolitan area includes New York City, Long Island, and the Mid and Lower Hudson Valley in the state of New York; the five largest cities in New Jersey: Newark, Jersey City, Paterson, Elizabeth, and Edison, and their vicinities; six of the seven largest cities in Connecticut: Bridgeport, New Haven, Stamford, Waterbury, Norwalk, and Danbury, and their vicinities.

- In a 25 mile radius, there are 13,517,045 people with 6,650,741 in the labor force.

The wider benefit

I caught up this week with Jon Cozens who took former CEO Greg Bafalis’ place earlier this year, and he clarified and focused some of the broader-scale benefits and the runway forward.

Ambition. 4 plants in 4 years at this scale. So think, overall, diversion of 500,000 tons of biosolids from landfills.

PFAS. Yes, those forever chemicals, they are in biosolids, and gasification at the temperature that Aries operates appears to be ideal to destroy them. To render them non-forever chemicals. That’s terrific news.

Landfilling biosolids. Jon Cozens reminds me that it’s getting to find facilities that accept them for lots of reasons and PFAS is among them. Long-term, that means that supply for technologies such as ACT’s is likely to rise, and anxiety amongst aggregators of sludge is only going to increase. The price of supply is trending down, the alternative cost to haul and landfill is going up. Some bans are in place. Maine is considering one.

Expansion. Right now, ACT has low-carbon technology, but there are opportunities to get to carbon zero or negative carbon intensity. And, the company will shift to a modular construction system to reduce capex and gain deployment speed.

Low capex. The Linden facility — and think of that as the higher end cost — was costed at $65M and $50M was raised through New Jersey county bonds. So, think $500 capex per ton of feedstock, that’s vastly smaller amounts than large integrated biorefineries that are often on the search for high nine-figure sums; several in the billions.

Low complexity business case. Leaving aside some small value int he heat, power and fly ash, the main source of business viability are tipping fees. Biosolids have to go somewhere, they are not the product of some kind of wasteful practice than can be reduced, they can’t be avoided, they don;t drop in volume during recessions. So, those tipping fees are likely more stable than what we might see for MSW fees for biorefineries. In the end, that’s the heart of the business case, ACT acts as a converter of biosolids, but in the end competes with the storage solution of the landfill. Just have to be cheaper than that.

Interesting value chain. No competition with haulers, Cozens told The Digest. The haulers will be business partners — they aggregate as they always have, pay the standard tipping fee just as they would at the landfill, only they can haul it less and have a destination that doesn’t fill up of get banned.

Compelling long-term value uplift. ACT confirmed that they are not signing those 20-year supply agreements beloved by investors; much more short-term in character. The reason? There may be quite a bit of shrinkage in landfill opportunities for biosolids — if you can’t dispose and you have PFAs issues, to boot, then the sky is the limit on value.

Things Yet to See Before Exaltation Begins

OK, the plant is late, over budget, and has had more issues than expected in getting it running. Mechanical completion was announced in November 2021. Yikes, that’s a long optimization period; another of these gasification-is-more-difficult-to-perfect-than-we’d-like stories. Let me share an equation I learned some time ago.

1/(LATENESS * COST OVERRUN) = INVESTOR SHORT-TERM CONFIDENCE

In this case, jury’s going to be out on the expansion plan until solid (or should I say, biosolid) performance is seen this year. If you can make solids out of liquids and solidly and reliably, your financials will be more solid and your position more liquid.

The Bottom Line

Aries is almost, almost, almost there. We’ll have Jon Cozens on the ABLC NEXT stage in October and I think we should have the answers then. If it goes as expected, then here’s this low capex tech with a modular construction plan, an almost limitless supply of negative-cost feedstock, and a straightforward business case. Let’s not forget the hydrogen in the syngas either. This one is a little like starting at Vesuvius, you’re not sure when it will erupt, but when it does it’ll be a doozy.